PT 360 Economy April 2024: UPSC 2025

Tip: For reading free UPSC Prelims 2025 Current Affairs for Economy online, use the Next/Previous buttons or refer to the Sidebar. If you are using a mobile device, click the menu icon (three horizontal lines) to access the sidebar.

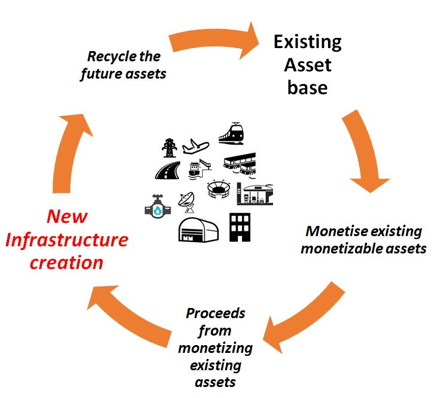

ASSET MONETIZATION

News Context

- The National Highway Authority of India (NHAI) recently achieved its highest monetization value to date, totaling ₹15,624.9 crore, using the Infrastructure Investment Trust (InvIT) model.

About Asset Monetization (AM)

- Origin: The concept of Asset Monetization was initially proposed by a committee chaired by economist Vijay Kelkar in 2012. It was later introduced in the Union Budget for 2021-22 through the National Monetisation Pipeline.

- Asset Monetization refers to the process of generating new revenue streams for the government and its agencies by realizing the economic potential of public assets that are either unused or underused. This can include any property owned by a public entity, such as roads, airports, and pipelines.

- Governance: A designated Core Group of Secretaries on Asset Monetization (CGAM), chaired by the Cabinet Secretary, has been established to oversee and manage the implementation of the project.

- Mechanism of Asset Monetization:

- Asset Monetization entails leasing or licensing a government-owned asset to a private sector company for a predetermined duration.

- The rights transfer in return for payments is regulated by a concession agreement, which ensures equitable risk-sharing between the public authority and the private entity.

Infrastructure Asset Monetisation cycle

Initiatives taken for Asset Monetization

- National Monetisation Pipeline (NMP):

- Sectors: The government has pinpointed 13 sectors for the monetization of its brownfield infrastructure assets. The five primary sectors account for approximately 83% of the overall pipeline: Roads (27%), Railways (25%), Power (15%), Oil & Gas pipelines (8%), and Telecom (6%).

- Potential: There is a monetization potential of ₹6.0 lakh crores from the core assets of the Central Government, projected over four years from FY 2022 to FY 2025.

- Specific Assets/Asset Classes for Monetization:

- Railways plan to monetize Dedicated Freight Corridor assets for operational and maintenance purposes after their commissioning.

- Airports are set to be monetized through operations and management concessions.

- National Land Monetization Corporation: This Special Purpose Vehicle (SPV) is established to handle the monetization of surplus land owned by Central Public Sector Enterprises (CPSEs) and other government bodies.

- Asset Monetization Dashboard: A tool created to monitor progress and enhance visibility for investors.

ASSET RECONSTRUCTION COMPANIES

NEWS CONTEXT

- RBI issues master Direction for Asset Reconstruction Companies

- Issued under powers from SARFAESI Act, 2002

- Applicable to all ARCs registered with RBI under Section 3 of the SARFAESI Act, 2002

- Aim is to streamline and regulate ARCs in India

- Ensure transparency, accountability, and integrity in the financial system.

About Asset Reconstruction Companies (ARCs)

- An ARC is a financial entity that acquires Non-Performing Assets (NPAs) or distressed assets from banks and financial institutions, enabling them to improve their balance sheets. ARCs must resolve these assets within a maximum period of eight years after acquiring them and redeem the Security Receipts (SRs) associated with the assets.

- Genesis: The SARFAESI Act of 2002 established the framework for the registration and regulation of ARCs by the Reserve Bank of India (RBI). As of 2022, there are 29 ARCs operating in India. The Narsimham Committee II (1998) recommended the creation of asset reconstruction companies, drawing inspiration from global asset management companies.

- Types: ARCs can be categorized based on ownership into public, private, or public-private partnerships.

- Examples: Notable ARCs include the National Asset Reconstruction Company Limited (NARCL) and the India Debt Resolution Company Ltd.

How ARCs Work?

- Asset Acquisition: ARCs purchase financial assets from banks or financial institutions, either holding them on their own books or in a trust for securitization or reconstruction purposes.

- Security Receipts: Lenders sell distressed loans to ARCs at a reduced price. When the transaction is not entirely in cash, ARCs issue security receipts that can be redeemed as the specific loan is recovered.

- Management Fee: ARCs charge a management fee of 1.5% to 2% of the asset value annually to the sellers of bad loans.

Key Provisions of Master RBI (ARCs) Directions, 2024

- Net Own Fund (NOF): An Asset Reconstruction Company (ARC) must maintain a minimum NOF of ₹300 crore to start its securitisation or asset reconstruction operations, with this requirement continuing thereafter.

- Registration: Prior to beginning its securitisation or asset reconstruction activities, an ARC must apply for and secure a certificate of registration (CoR) from the RBI.

- Leadership Positions: The guidelines establish a maximum age of 70 for the Managing Director/Chief Executive Officer or Whole-time Director, along with a tenure limit of five years per term, which can extend to a maximum of 15 years in total.

- Reporting Obligations: ARCs are required to report to the Indian Banks’ Association (IBA) any details regarding chartered accountants, advocates, and valuers who have engaged in significant professional misconduct, for inclusion in the IBA database.

- Internal Audit: ARCs must implement a robust internal control system that includes regular checks and reviews of asset acquisition processes and reconstruction activities.

- Additional Provisions:

- ARCs are not allowed to raise funds through deposits.

- They must maintain a capital adequacy ratio of at least 15% of their total risk-weighted assets.

Other recent changes by RBI in ARCs Regulations

- Strengthened corporate governance: RBI mandated that the chair of the board and at least half the directors in a board meeting must be independent directors.

- Increased transparency: ARCs must disclose their track record on returns generated for security receipt investors and engage with ratings agencies of schemes floated in the last eight years.

- Fair Practices Code (FPC): ARCs are advised to put in place a Board-approved FPC to achieve the highest standards of transparency and fairness.

- Membership of CIC: Every ARC must become a member of at least one credit information company (CIC) registered with the RBI.

ADVANCE PRICING AGREEMENTS (APAS)

News Context

In the fiscal year 2023-24, the Central Board of Direct Taxes (CBDT) has set a new record by signing 125 APAs (including both Unilateral and Bilateral APAs) with Indian taxpayers.

About Advance Pricing Agreements (APAs)

Overview of Advance Pricing Agreements (APAs)

- An APA is a contract between a taxpayer and the relevant tax authority.

- The primary goal of APAs is to provide taxpayers with certainty in transfer pricing by outlining specific pricing methods.

- It allows for the determination of the arm’s length price (ALP) for international transactions in advance, covering a period of up to five years into the future.

- Additionally, taxpayers have the option to roll back the APA for four previous years, offering tax certainty for a total of nine years.

Categories of APAs

- Unilateral APA: This type involves only the taxpayer and the tax authority in the taxpayer's country.

- Bilateral APA: This includes the taxpayer, the tax authority of the taxpayer's country, and an associated enterprise (AE) in another country, along with the corresponding foreign tax authority.

- Multilateral APA: This involves the taxpayer, two or more AEs in different countries, the tax authority of the taxpayer's country, and the tax authorities of the AEs.

Mutual Agreement Procedure (MAP):

- MAP offers taxpayers a means to address disputes related to double taxation, whether they are of a legal or economic nature.

- It is a process outlined in tax treaties (e.g., Double Taxation Avoidance Agreements, or DTAAs) to ensure that taxation aligns with the stipulations of the treaty.

- A tax treaty is a bilateral agreement between two countries aimed at resolving issues concerning the double taxation of both passive and active income earned by their citizens.

- Key distinctions between MAP and Advance Pricing Agreements (APAs):

- MAP deals with resolving existing transfer pricing disputes, whereas APAs are designed to prevent such disputes from arising.

- Taxpayers utilize MAP for ongoing disputes, while they seek APAs for the same transactions in future years as a proactive strategy for dispute resolution and avoidance.

Indian Advance Pricing Agreement Regime:

- APA Scheme in India:

- The Ministry of Finance introduced the APA Scheme in 2012 by adding sections 92CC and 92CD to the Income-tax Act, 1961.

- The rules for APA were later issued by the Central Board of Direct Taxes (CBDT).

- This scheme involves an agreement between the CBDT and an individual or entity to establish an arm's length price for international transactions in advance.

- The Ministry of Finance introduced the APA Scheme in 2012 by adding sections 92CC and 92CD to the Income-tax Act, 1961.

- Nature of the Scheme:

- The APA process is voluntary and acts as a complementary mechanism to appeals and other Double Taxation Avoidance Agreements (DTAAs) for resolving transfer pricing disputes.

- Term of APA: The maximum duration of an APA is five years.

- Rollback Provisions: This allows the agreed arm's length price in the APA to be applied retroactively to a period before the APA's effective start date.

Central Board of Direct Taxes

- Establishment: CBDT was created under the Central Board of Revenue Act, 1963.

- Ministry: It operates within the Department of Revenue under the Ministry of Finance.

- Functions: CBDT plays a key role in shaping policies and planning related to direct taxes in India. It also oversees the enforcement of direct tax laws through the Income Tax Department.

- Composition: The CBDT is made up of a Chairman and six Members who are responsible for its operations and decision-making.

Related News Double Taxation Avoidance Agreement (DTAA)

- India and Mauritius have signed a protocol to amend the Double Taxation Avoidance Agreement (DTAA), which is pending ratification.

- The amendment introduces a Principal Purpose Test (PPT) to prevent the misuse of the treaty for tax evasion and avoidance.

- The PPT stipulates that tax benefits from the treaty will not apply if obtaining such benefits was the primary aim of any transaction or arrangement.

- This protocol aims to ensure compliance with the Minimum Standards of Base Erosion and Profit Shifting (BEPS).

- The DTAA is designed to prevent double taxation of the same income or asset across two countries or territories.

- The initial agreement between India and Mauritius was signed in 1982 and amended in 2016.

Significance of the DTAA:

- Facilitates cross-border investments by lowering the tax burden on foreign investors.

- Ensures a fair distribution of tax rights between the source and residence countries.

- Offers legal clarity regarding the taxation of international income.

Issues Related to the DTAA:

- Treaty Shopping: Occurs when individuals from a non-party country exploit the treaty’s provisions through indirect means.

- Double Non-Taxation: The misuse of the DTAA can lead to situations where taxes are avoided in both nations.

- Differential Interpretations: Varying understandings of tax treaties can result in lengthy legal disputes.

Base Erosion and Profit Shifting (BEPS):

- Involves using loopholes in tax laws to avoid paying taxes by moving profits to lower tax areas

- The Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS is designed to update tax rules internationally and reduce opportunities for tax avoidance by large companies.

- India became a signatory to the convention in 2017.

BASEL III ENDGAME

News Context

- CBA released a White Paper on the impact of the Basel III Endgame Proposal

- The focus is on consumers on the margins of the U.S. financial system

- The paper discusses how the proposal will affect these consumers

- It highlights potential challenges and implications for this group of consumers

About Basel III Endgame

Basel III Endgame Overview

- Basel III Endgame refers to the final set of rules of Basel III norms developed by the Basel Committee on Banking Supervision.

- The purpose of Basel III is to strengthen the regulation, supervision, and risk management of banks.

Impact of Basel III Endgame

- Globally Systemically Important Banks (G-SIBs) may see a 21% increase in capital requirements.

- The proposed changes aim to enhance the strength and resiliency of the banking system.

- Transparency and consistency in banks' capital frameworks are also expected to improve with the implementation of Basel III Endgame.

Basel Committee on Banking Supervision

- Establishment: Founded by central bank Governors of G10 countries in 1974

- Members: Consists of 45 members including central banks and bank supervisors, with the RBI being one of its members

- Functions:

- Enhancing financial stability by improving banking supervision globally

- Serving as a platform for collaboration among member countries on banking supervisory issues

- Governance: Reports to oversight body "Group of Central Bank and Governors and Heads of Supervision (GHOS)"

- Implementation of decisions: Decisions made by BCBS do not have legal authority

Basel Norms (See the box at the end of this article for key terminologies related to Basel Norms):

- Overview: These regulations emphasize the required capital that banks must maintain to cover credit, operational, and market risks associated with their operations.

- Banks encounter substantial risks, primarily because they are one of the most leveraged sectors.

- Highly leveraged sectors depend significantly on debt to finance their operations and investments.

- Basel I Norms (1987):

- In 1987, the Committee established a capital measurement system that concentrated on credit risk and the risk-weighting of assets.

- These norms defined the minimum capital requirements that banks should maintain.

- Basel II Norms (2004):

- These revised norms aimed to enhance risk assessment in capital measurement by introducing three key pillars: Minimum capital requirements, Supervisory Review, and Market Discipline.

- Basel III Norms (2010):

- Issued in response to the financial crisis of 2007-08.

- The objective is to establish a strong capital base for banks and ensure stable liquidity and leverage ratios.

Key Features of Basel I, II and III Compared

Pillar I (Capital Requirements)

- Basel I: At least 8% minimum ratio of capital to RWAs

- Basel II: 8% Tier 1 capital to RWAs

- Basel III: 8% + 2.5% of Capital Conservation Buffers, 6% Tier 1 capital to RWAs

Pillar II (Supervisory Review Process)

- Basel I: No provisions for Supervisory Review

- Basel II: Risk Based Supervision introduced

- Basel III: Enhanced Supervisory Process

Pillar III (Disclosure & Market Discipline)

- Basel I: No provisions related to Market Discipline

- Basel II: Quantitative and Qualitative disclosures prescribed at Quarterly, Half-Yearly and Yearly intervals

- Basel III: Enhanced Disclosure Norms

New Banking Capital Requirement Parameters Introduced by Basel III

Capital Conservation Buffers to RWAs: 2.5%

- Leverage Ratio: 3%

- Counter Cyclical Buffer: 0% to 2.5%

- Minimum Liquidity Coverage Ratio: ≥100%

- Minimum Net Stable Funding Ratio: ≥100%

Implementation of Basel Norms in India:

- The Reserve Bank of India (RBI) introduced Basel I norms in its Mid-term Review of Monetary and Credit Policy for 1998-99, raising the Capital to Risk-Weighted Assets Ratio (CRAR) from 8% to 9%.

- In 2007, the RBI released the final guidelines for the implementation of Basel II.

- Draft guidelines for Basel III capital regulations were published in December 2011.

- The Basel III capital regulations (Pillar I of Basel III Norms) were put into effect in India starting April 2013 and were fully implemented by October 2021.

- The norms set by the RBI are more stringent and prudential compared to the original Basel norms.

CLUSTER DEVELOPMENT PROGRAMME (CDP) – SURAKSHA

- States using SURAKSHA platform for horticulture subsidies

- CDP is part of National Horticulture Board scheme

- About

- SURAKSHA stands for 'System for Unified Resource Allocation, Knowledge, and Secure Horticulture Assistance'

- Instant subsidy disbursal to farmers through e-RUPI voucher from NPCI

- Features include database integration, UIDAI validation, geotagging, geo-fencing

- Access for farmers, vendors, Implementing Agencies, Cluster Development Agencies

CONSUMER CONFIDENCE SURVEY

News Context

The most recent round of the bi-monthly Consumer Confidence Survey (CCS) was released by the Reserve Bank of India (RBI) in January 2023.

About Consumer Confidence and the Consumer Confidence Survey (CCS)

- The CCS is an economic indicator that assesses consumers' optimism or pessimism regarding the overall economy and their personal financial situations.

- It reflects the economic health from the consumers' viewpoint.

- High consumer confidence often correlates with increased consumer spending.

- Measurement: The Reserve Bank of India (RBI) conducts a bi-monthly CCS to gauge consumer sentiment.

- The survey captures current perceptions compared to a year ago and expectations for the upcoming year across 19 major cities.

- It gathers insights into urban consumer sentiments and includes qualitative responses regarding the general economic climate.

- Index Metrics: The CCS is evaluated through two indices:

- Current Situation Index (CSI): Measures consumer sentiment regarding current economic, employment, and price conditions relative to a year prior.

- Future Expectation Index (FEI): Gauges expectations for economic, employment, and price conditions for the year ahead.

- Businesses utilize these insights to make informed decisions and strategize, including investments and new product launches.

Findings from the Latest Consumer Confidence Survey

- Overall Improvement: Consumer confidence has increased for both the current period and future expectations.

- Current Situation Index (CSI): The CSI continues to recover from its historic low in mid-2021, driven by enhanced sentiments regarding the general economic situation and household income.

- Future Expectations Index (FEI): The FEI reached a two-year high, reflecting greater optimism about the economic outlook, employment prospects, and income over the next year.

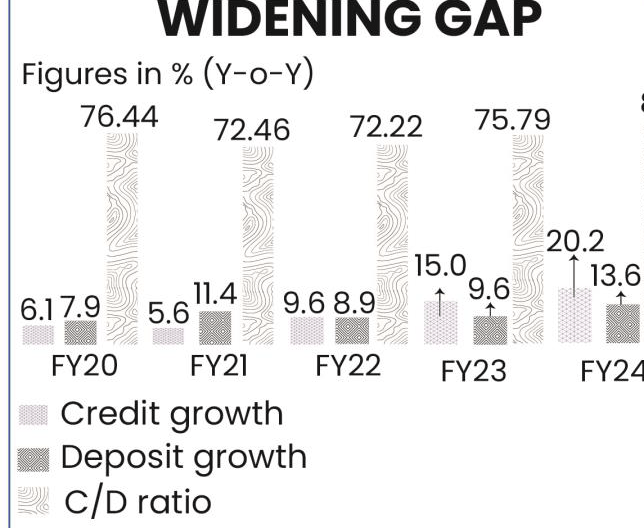

CREDIT DEPOSIT RATIO (CDR)

- Indian banks are facing their most severe deposit shortage in two decades, with a credit-deposit ratio (CDR) of 80%, the highest level since 2005.

- About CDR:

- This ratio indicates the proportion of a bank's loans relative to its total deposits.

- A higher CDR means that a large share of the bank's funds is being used for loans, which can promote economic growth but also increases risk.

- Regulators typically monitor CDR to ensure that banks strike a careful balance between lending activities and risk management.

EXPERT COMMITTEE REPORT ON GIFT CITY

- The Expert Committee tasked with transforming GIFT IFSC into a "Global Finance and Accounting Hub" has submitted its report to the IFSCA.

- This committee was established following a notification from the Ministry of Finance.

- The notification categorized bookkeeping, accounting, taxation, and financial crime compliance as "financial services" under the International Financial Services Centre (IFSC) Act of 2019.

- The Gujarat International Finance Tech-City (GIFT City) - IFSC was established as a Special Economic Zone (SEZ) in Gujarat in 2015.

- An IFSC serves clients outside the domestic economy, facilitating the movement of financial resources, products, and services across international borders.

- Potential for GIFT IFSC to emerge as a Global Finance and Accounting Hub includes:

- Robust technology-driven outsourcing capabilities.

- A vast pool of skilled professionals in accounting and related fields.

- "Accounting and finance services" are recognized as one of the 12 Champion sectors for service exports.

- Recommendations:

- Introduce new regulations to define bookkeeping, accounting, taxation, and financial crime compliance services comprehensively and inclusively.

- Only companies or limited liability partnerships registered should be permitted to provide these services.

- Develop long-term strategies for education and skill development, including specialized degree or diploma programs.

- IFSC Authority:

- The IFSC Authority is a statutory body formed under the IFSC Act of 2019.

- It acts as a unified regulator for the development and regulation of financial products, services, and institutions within IFSCs in India.

FINANCING FOR SUSTAINABLE DEVELOPMENT REPORT 2024

News Context

The Inter-agency Task Force on Financing for Development recently published the 2024 Financing for Sustainable Development Report.

About Inter-Agency Task Force on Financing for Development

- The initiative includes more than 60 UN agencies, programs, offices, regional economic commissions, and other international institutions.

- The UN Department of Economic and Social Affairs (UNDESA) is responsible for coordinating the initiative.

- The initiative was established by the UN Secretary General to monitor and implement the seven action areas outlined in the Addis Ababa Action Agenda.

Action Areas

- Utilizing resources within a country for public use

- Involvement of private businesses and finance from both domestic and international sources

- Collaboration with international development partners for support

- Using international trade to drive economic growth

- Ensuring debt levels are manageable for sustainable development

- Tackling underlying systemic problems

- Investing in science, technology, innovation, and building capacity for development.

Key highlights of the report

- Progress Toward SDGs: Many countries are not on track to meet the 2030 Agenda for Sustainable Development, with approximately half of the 140 SDG targets showing significant deviations from the necessary trajectory.

- Financing Gaps in Sustainable Development: The report estimates that the financing and investment shortfalls needed for the SDGs range between USD 2.5 trillion and USD 4 trillion each year.

- Finance Disparities: Developing nations face considerably poorer conditions for accessing both long-term and emergency financing, with the most significant gaps occurring in Middle-Income Countries (MICs).

- Weak Support for SDGs: Public subsidies and private investments in fossil fuels and environmentally harmful activities remain excessively high at present.

About Financing for Sustainable Development

- This initiative focuses on facilitating the follow-up to agreements and commitments made regarding Financing for Development during:

- The 2002 conference in Monterrey, Mexico;

- The 2008 conference in Doha, Qatar; and

- The 2015 conference in Addis Ababa, Ethiopia.

- The Addis Ababa Action Agenda establishes a new global framework for financing sustainable development.

- It ensures that all financing flows and policies align with economic, social, and environmental priorities, promoting stability and sustainability in funding.

- The agenda outlines seven key action areas for financing sustainable development (refer to infographic).

- It requires the Task Force to:

- Provide annual reports on the progress of implementing the Addis Agenda and other Financing for Development outcomes, as well as the means for achieving the 2030 Sustainable Development Agenda.

- Offer guidance on the intergovernmental follow-up process regarding progress, implementation gaps, and recommendations for corrective actions.

- The Addis Ababa Action Agenda was adopted during the Third International Conference on Financing for Development, which took place in Addis Ababa, Ethiopia, in 2015.

- Financing challenges are central to the ongoing crisis in sustainable development.

Actions required for bridging financing gap for sustainable development

- Creating an Enabling Environment: Countries should align their initiatives to foster private investment with the Sustainable Development Goals (SDGs) by establishing appropriate incentives through fiscal and tax policies.

- Enhancing Public Development Banks (PDBs): PDBs typically offer long-term financing and their focus on development allows their lending terms to better support social and environmental sustainability.

- Adopting Integrated Financing Approaches: Over 80 countries are currently implementing Integrated National Financing Frameworks (INFFs) to formulate national financing strategies that merge planning with financing policies. The concept of INFFs was initially introduced in the Addis Agenda.

- Reforming the Multilateral System: It is essential to implement reforms that improve the synergy between trade, investment, and sustainable development. This includes necessary changes to the World Trade Organization (WTO), particularly in dispute resolution, updating regulations to align with current global economic realities, and ongoing revisions of investment treaties.

GLOBAL UNICORN INDEX 2024

News Context

- Hurun research group released the 'Global Unicorn Index 2024'

- The index focuses on unicorn companies around the world

- It provides insights into the top unicorn companies and their growth prospects

- The index is a valuable resource for investors and analysts tracking unicorn companie

Key Findings of the Report:

- India had 67 unicorn startups in 2023, ranking third globally behind the USA and China.

- Indian founders produced more offshore unicorns than domestic ones.

- A unicorn startup is privately held, valued at $1 billion or more, and supported by venture capital.

- Gazelles are startups likely to become unicorns within 3 years, while Cheetahs are likely to do so within 5 years.

Measures to be Taken:

- Sustainable Business Models: Unicorns should focus on achieving profitability instead of merely pursuing rapid growth, while also investing in technology and innovation and exploring diverse revenue sources.

- Fair Valuation: Improved regulation of valuation practices is necessary.

- Regulatory Environment: Streamlining and rationalizing legal and compliance processes can foster stability and build confidence among Unicorns for the future.

GROSS FIXED CAPITAL FORMATION (GFCF)

News Context

- The slow growth of private Gross Fixed Capital Formation (GFCF) as a percentage of Gross Domestic Product (GDP) is a major issue for the Indian economy.

Evolution of GFCF (also called Investment):

- Investment levels in India have fluctuated over the years, with it hovering around 10% of GDP from independence to economic liberalization.

- There was a significant increase in investment from the 1980s to 2007-08, reaching around 27% of GDP.

- However, private investment started to decline from 2011-12 onwards, hitting a low of 19.6% of GDP in 2020-21.

- In terms of absolute numbers, GFCF in the Indian economy increased from Rs. 32.78 lakh crore in 2014-15 to Rs. 54.35 lakh crore in 2022-23 (Provisional Estimates).

Reasons for fall in Private GFCF:

- Historical trend of higher consumption leading to lower private investment in India

- Unfavorable government policies and policy uncertainty, such as disputes related to tax laws

- Slowdown in the pace of reforms in the last two decades leading to a drop in private investment

What are Capital Formation (CF) and Gross Fixed Capital Formation (GFCF)?

- Capital formation is the process of investing resources in assets like plants, equipment, machinery, and human capital through education, health, and skill development.

- Gross Capital Formation (GCF) refers to the growth in the size of fixed capital in an economy, which includes Gross Fixed Capital Formation (GFCF), change in stock of raw materials, semi-finished and finished goods, and net acquisition of valuables.

- Gross Fixed Capital Formation (GFCF) specifically includes investments in land improvements, plant, machinery, equipment purchases, and construction of infrastructure like roads.

- Change in stock (CIS) refers to the stocks of goods held by firms to manage temporary fluctuations in production or sales.

- Net acquisition of valuables includes investments in items like gold, gems, ornaments, and precious stones.

- Net capital formation (NCF) differs from GCF as it takes into account depreciation, obsolescence, and accidental damage to fixed capital.

| Included in GFCF | Not included in GFCF |

|---|---|

| Infrastructure such as airports and roads | Intangible assets like software or artistic originals |

| Livestock that is used repeatedly, such as dairy cattle and sheep | Transactions intended as intermediate consumption |

| Cultivated crops that are harvested repeatedly | Machinery and equipment intended for household final consumption expenditure |

| Major repair and maintenance that extends the economic life of assets | Losses due to natural disasters such as flooding or forest fires |

Why GFCF is an important economic variable?

- Growth Multiplier: GFCF and GDP have a positive correlation, meaning that an increase in GFCF leads to an increase in GDP.

- Boosts Productivity and Living Standards: GFCF helps workers produce more goods and services, leading to higher output and improved living standards.

- Promotes Self-sufficiency: Growth in GFCF allows for the creation of capital assets, improving self-sufficiency in production and research in the long term.

- Indicator of Market Confidence: GFCF is a meaningful indicator of future business activity, business confidence, and economic growth patterns.

- Private GFCF can indicate the willingness of the private sector to invest in the economy.

- Reflects Overall Output: GFCF helps determine the overall output of an economy, influencing what consumers can purchase in the market.

What is hindering the growth of GFCF?

- Slow pace of reforms, particularly in land acquisition, discouraging investors from investing in the economy

- Financial problems faced by Indian banks and large corporations, leading to capital being locked in the market and not reinvested in new projects

- High cost of borrowing, slowing down the lending and borrowing cycle and hindering effective investment channeling

- High cost of borrowing is influenced by higher lending rates, which are impacted by high inflation.

HIGH INCOME AND WEALTH INEQUALITY IN INDIA

News Context

- Numerous studies have highlighted the significant disparity in income and wealth in India, sparking discussions on economic inequality and the unequal distribution of wealth.

Economic Inequality in India

- Wealth Inequality: India has high wealth inequality, with the rich getting richer at a faster rate than the poor.

- Income Inequality: The top 1% in India received 22.6% of the national income, which is among the highest in the world.

- Rural-Urban Divide: There is a significant difference in average monthly per capita consumption expenditure between rural and urban India.

- Gender Pay Gap: There is a noticeable difference in pay between men and women in India.

Key findings of oxford report:

- Top 1% income shares have increased.

- Share of income for the bottom 50% has declined.

- The top 5% of Indians own more than 60% of the country's wealth

Measures Undertaken to Reduce Economic Inequality

- Inclusive Growth Initiatives: Deendayal Antyodaya Yojana-National Rural Livelihood Mission aims to reduce poverty by providing self-employment and wage employment opportunities to poor households.

- Other Initiatives: Mahatma Gandhi National Rural Employment Guarantee Yojana, Pradhan Mantri Awas Yojana, Skill India Mission, etc.

- Financial Inclusion Initiatives: PRADHAN MANTRI JAN-DHAN YOJANA ensures access to financial services like banking, savings, insurance, remittance, etc.

- Other Initiatives: Pradhan Mantri Mudra Yojana, Stand-Up India Scheme, etc.

- Social Security Measures: Atal Pension Yojana provides old age income security for the unorganized sector.

- Other Initiatives: Pradhan Mantri Suraksha Bima Yojana (Accident Insurance), Pradhan Mantri Jeevan Jyoti Yojana, etc.

- Promoting Gender Equality: Beti Bachao Beti Padhao Scheme aims to prevent gender biased sex selective elimination and ensure education and participation of the girl child.

- Other Initiatives: One Stop Centre Scheme, SWADHAR Greh, Pradhan Mantri Matru Vandana Yojana, etc.

- Sustainable Development Initiatives: National Mission for Sustainable Agriculture aims to make agriculture more productive, sustainable, and climate resilient.

- Other Initiatives: National Mission on Enhanced Energy Efficiency, National Action Plan on Climate Change, etc.

Impact of Economic Inequality

- Economic inequality has a significant impact on various aspects of society

- Social unrest and conflict can arise due to disparities in wealth and opportunities

- Reduced social mobility means that individuals have limited chances to improve their economic situation

- Environmental degradation may occur as a result of unequal distribution of resources and access to sustainable practices

- Poverty and deprivation can be perpetuated when economic inequality is not addressed

- Human development is hindered when individuals do not have equal access to education, healthcare, and other essential services

- Political instability can arise when there is a large gap between the rich and the poor

- Economic growth may be slowed down when resources are not distributed equitably among the population.

INTERNATIONALIZATION OF RUPEE

News Context

- Prime Minister requested RBI to create a 10-year plan for making the Indian rupee a globally recognized currency

- Goal is to increase accessibility and acceptance of the rupee on an international scale

- Aim is to facilitate the internationalization of the Indian currency

About Currency Internationalization

- An international currency is utilized and held beyond the issuing nation's borders, not only for transactions involving residents of that country but also for exchanges between non-residents.

- Currency internationalization refers to the global expansion of a national currency's three fundamental roles: serving as a unit of account, a medium of exchange, and a store of value.

- Currently, the primary reserve currencies worldwide include the US dollar, Euro, Japanese yen, and pound sterling.

- In the late 1990s, India began moving towards partial convertibility and has since made strides through various reforms.

- This includes allowing capital-account transactions, such as enabling corporate entities to raise funds via external commercial borrowings and Masala bonds (rupee-denominated bonds issued by Indian entities abroad).

Determinants of Internationalization of currency

- Economic fundamentals play a significant role in the internationalization of a currency, including the size of the economy and the strength of its trade network.

- The depth and liquidity of capital markets also impact the internationalization of a currency, as these factors can make it easier for foreign investors to buy and sell the currency.

- The stability and convertibility of a currency are crucial determinants of its internationalization, as a stable and easily convertible currency is more likely to be used in international trade and investment.

Approach for the Internationalization of the Rupee

- Capital Account Convertibility: The Indian National Rupee (INR) is fully convertible in the current account but only partially in the capital account.

- There is a need to reassess the existing provisions of the Foreign Exchange Management Act (FEMA) and to enhance incentives for conducting international trade settlements in INR.

- Facilitate banking services (such as loans, guarantees, credit lines, etc.) in INR through the offshore branches of Indian banks.

- Promoting the International Use of INR: To support international financial transactions in INR, it is essential to establish an effective settlement mechanism, ensure liquidity availability, and develop a strong cross-border payments system.

- Currency Swaps and Local Currency Settlement (LCS): These mechanisms promote currency diversification, stabilize the local currency, shield businesses from currency risk, and lower transaction costs.

- Internationalization of Indian Payment Systems: Expand the global reach of India's payment systems, including Real Time Gross Settlement (RTGS), National Electronic Funds Transfer (NEFT), and Unified Payments Interface (UPI).

- Inclusion of INR in Continuous Linked Settlement (CLS): CLS is a worldwide system for settling foreign currency transactions on a Payment vs Payment (PvP) basis. Currently, it operates for 18 currencies, excluding INR.

- Establishment of an Indian Clearing System: This system would offer member banks a marketplace for purchasing currencies against their domestic currency.

- Positioning INR as a Vehicle Currency and Potential Inclusion in the Special Drawing Rights (SDR) Basket: This can be achieved by promoting trade invoicing in INR and strengthening trade relations with other economies.

- Strengthening Financial Markets:

- Harmonization of KYC (Know Your Customer) Norms: Aligning the KYC regulations of the RBI and SEBI to simplify foreign investors' access to INR-denominated assets.

- Global 24x5 INR Market: While customer transactions can occur round-the-clock in the offshore market, the onshore inter-bank market is limited to specific hours.

- Inclusion of Indian Government Bonds in Global Bond Indices: This will broaden the investor base, ensure stable passive inflows, enhance the value of INR, and lower overall borrowing costs.

Steps taken towards internationalization of Rupee

- Utilization of Indian Payment Infrastructure: India has connected UPI with Singapore's PayNow and is working on expanding its reach globally.

- Special Vostro Rupee Accounts (SVRAs): RBI has established a system for INR trade settlement with 22 countries through SVRAs.

- INR as a Designated Foreign Currency in Sri Lanka: This allows for bilateral trade to be conducted in INR.

- Asian Clearing Union (ACU): RBI has proposed including INR as a settlement currency under the ACU.

- Developments in Gujarat International Finance Tec-City (GIFT City): GIFT City is home to international exchanges and a depository.

- Bilateral Swap Arrangements (BSA): India has a BSA with Japan and recently signed a currency swap agreement with UAE.

INHERITANCE TAX AS A TOOL OF WEALTH REDISTRIBUTION

News Context

- Inheritance tax is a tax levied on property or assets inherited upon an individual's death, different from estate tax.

- Countries like Japan and South Korea have inheritance tax systems with high tax rates.

What is Inheritance Tax?

- Inheritance tax is a tax imposed on property or assets received by an individual after someone's death.

- It is distinct from estate tax, which is imposed on the total value of a deceased person's estate.

- Many countries levy inheritance tax, with varying tax rates such as Japan (55%) and South Korea (50%).

History of Inheritance Tax in India

- Inheritance tax is currently not applicable in India

- Estate duty was introduced in 1953 with tax rates as high as 85%, but was abolished in 1985 due to unpopularity

- Gift tax and wealth tax were also imposed in India, but were abolished in 1998 and 2015 respectively

- Gift tax was reintroduced in 2004, with gifts exceeding Rs 50,000 in a financial year being added to the recipient's income and taxed accordingly

- Exceptions to gift tax include donations, inheritance, gifts from close relatives, and gifts during weddings.

INSURANCE REGULATORY AND DEVELOPMENT AUTHORITY OF INDIA (IRDAI)

News Context

The 25th Anniversary of the Insurance Regulatory and Development Authority of India (IRDAI) was commemorated.

Insurance Regulatory and Development authority of India (IRDAI)

Genesis

- Established based on recommendations of Malhotra Committee

- Became an autonomous body in 1999 and a statutory body in 2000 under the Insurance Regulatory and Development Authority Act, 1999

Objectives of IRDAI

- Ensure speedy and orderly growth of insurance industry

- Facilitate speedy settlement of genuine claims

- Provide an effective grievance redressal mechanism

- Focus on strengthening insurance customers, providers, and distributers

Ministry overseeing IRDAI

- Ministry of Finance is responsible for overseeing IRDAI

Composition of IRDAI

- Consists of a 10-member body including a chairman, five full-time members, and four part-time members

Role of IRDAI

- Issue, renew, modify, withdraw, suspend, or cancel registration for insurance providers

- Protect the interests of policyholders

- Adjudicate disputes between insurers and intermediaries

- Promote and regulate professional organizations in the insurance and reinsurance business

Recent Regulatory Governance Reforms by IRDAI

- IRDAI has consolidated 34 regulations into 6 regulations and introduced 2 new regulations for clarity and coherence in the regulatory landscape

- The IRDAI (Insurance Products) Regulations, 2024 have merged 6 regulations into a unified framework to help insurers respond to market demands and boost insurance penetration

- The IRDAI (Corporate Governance for Insurers) Regulations, 2024 aim to establish a strong governance framework for insurers

- The IRDAI (Registration, Capital Structure, Transfer of Shares & Amalgamation Insurers) Regulations, 2024 have streamlined 7 regulations into a single comprehensive framework to simplify processes and foster growth in the insurance sector

Major Initiatives by IRDAI

- Bima Sugam is an online platform for insurance transactions including buying, selling, servicing policies, and settling claims, part of IRDAI's Bima Trinity.

- Saral Jeevan Bima offers basic protection for self-employed individuals and those in low-income groups.

- The Integrated Grievance Management System aims to centralize grievances and analyze data to address policyholder concerns.

- A Pan India survey conducted by NCAER is helping improve insurance awareness strategies.

- Insurers are required to have a Board approved Insurance Awareness Policy with activities promoting consumer awareness.

Related News: Domestic Systemically Important Insurers (D-SIIs)

- The Insurance Regulatory and Development Authority of India (IRDAI) has published the 2023-24 list of D-SIIs.

- Life Insurance Corporation of India (LIC), General Insurance Corporation of India (GIC Re), and New India Assurance Company are recognized as D-SIIs.

- D-SIIs are insurers whose size, market significance, and interconnectedness, both domestically and globally, mean that their distress or failure could lead to substantial disruptions in the domestic financial system.

- These insurers are regarded as "too big or too important to fail" (TBTF).

- D-SIIs are subjected to enhanced regulatory oversight.

INDIA GAMING REPORT 2024 RELEASED

- Interactive Entertainment and Innovation Council (IEIC) and WinZO Launch India Gaming Report 2024

- Key Findings:

- India has become the largest gaming market in the world, boasting 568 million users, representing one in five online gamers globally.

- The Indian gaming market is projected to reach $6 billion by 2028.

- The number of gaming companies in India has skyrocketed from 25 in 2015 to over 1,400 in 2023.

- Factors Driving Growth in the Gaming Industry:

- Increased accessibility to affordable high-speed internet (priced at $0.17/GB) and a rise in smartphone usage (820 million users).

- A rapidly growing young population (~600 million) and an increase in disposable income.

- Supply-side factors include global investments in game development, the attractiveness of gaming careers, the availability of content in regional languages, and the incorporation of gaming elements into Indian culture.

- Gaming's Societal Contributions:

- Gaming helps reduce social isolation and fosters community building, particularly among women gamers, while also contributing to advancements in research, education, and skill development.

- It enhances the adoption of emerging technologies like Virtual Reality and Artificial Intelligence.

- Challenges Facing the Gaming Sector:

- Environmental sustainability concerns linked to "internet pollution," which accounts for 3.7% of global greenhouse gas emissions.

- Issues with financial literacy, regulatory challenges, and data security.

- Potential negative impacts on physical and mental health, as evidenced by cases such as the ‘Blue Whale Challenge.’

- Recommendations:

- Implement green technologies and virtual environments to promote sustainable gaming.

- Create a global gaming cluster supported by policies that nurture startups and talent development.

- Focus on research and development for online safety and digital literacy.

- Additional Information:

- The entity is registered as a company under the Companies Act of 1956/2013.

- Non-bank Payment Aggregators (PAs) must obtain authorization from the Reserve Bank of India under the Payment and Settlement Systems Act of 2007.

Government Initiatives to Support the Gaming Sector:

- MeitY oversees regulations and development of online gaming.

- Schemes such as Make in India, Digital India, and Production Linked Incentive (PLI) support the sector.

- Reports like the AVGC taskforce report, Draft National AVGC Policy, and National AVGC Centre of Excellence promote growth in the industry.

- 100% FDI is allowed in the gaming sector through automatic route within Electronic System and IT & BPM sectors.

LIVING WAGE AND MINIMUM WAGE

- The government has requested technical support from the ILO to establish a framework for a living wage.

- Currently, India adheres to a minimum wage policy that has not changed since 2017.

- The Wages Code, enacted in 2019, suggests a universal wage floor that will apply to all states once it is implemented.

Challenges with the Current System:

- The Minimum Wages Act of 1948 offers guidelines but does not define a specific minimum wage.

- Determining minimum wages for certain jobs is governed by both the Minimum Wages Act of 1948 and the Contract Labour (Regulation and Abolition) Act of 1970, which can create confusion.

- Wage discrepancies occur due to the absence of a nationally enforceable wage floor across different states.

- There is gender inequality in wages, as scheduled employment with a higher percentage of women workers tends to have lower minimum wages compared to those with more male workers.

Benefits of a Living Wage:

- It can enhance poverty alleviation efforts, supporting the Sustainable Development Goals (SDGs).

- It addresses wage insufficiency in light of inflation and promotes a fairer and more sustainable economy.

Challenges of Implementing a Living Wage:

- Establishing a national living wage framework across various states is complicated by the differences in living costs across regions in India.

- Small businesses and MSMEs may face financial pressure due to increased labor costs.

Difference between living wage and minimum wage

| Differential Aspects | Living Wage | Minimum Wage |

|---|---|---|

| Definition | The necessary wage needed for workers and their families to live comfortably | The lowest hourly pay rate required by law for employers to pay their employees |

| Aim | Enhancing the well-being of workers | Safeguarding workers from being taken advantage of. |

PRADHAN MANTRI FASAL BIMA YOJANA (PMFBY)

News Context

- In the 2023-24 fiscal year, the number of farmers enrolled in the PMFBY has reached a new high of over 40 million, showing a 27% increase from the previous year's 31.5 million enrollees.

- Claims Ratio: Approximately 5 times the premium amount is paid out as claims to farmers under PMFBY from 2016 to 2023.

- Claim Beneficiaries: More than 23.22 crore farmers have received claims under PMFBY since its implementation 8 years ago.

Objectives of PMFBY:

- To offer insurance protection and financial assistance to farmers in case of crop failure due to natural disasters, pests, or diseases.

- To stabilize farmers' incomes, ensuring their continued engagement in agriculture.

- To motivate farmers to embrace innovative and modern agricultural techniques.

Key Features of the Pradhan Mantri Fasal Bima Yojana (PMFBY) Launched in 2016:

- Objective: To provide comprehensive crop insurance covering the entire farming cycle from pre-sowing to post-harvest.

- Category: Central Sector Scheme.

- Character: Demand-driven and optional for both states and farmers.

- Implementing Body: The Department of Agriculture, Cooperation & Farmers Welfare (DAC&FW) under the Ministry of Agriculture & Farmers Welfare (MoA&FW), along with the respective state governments.

- Eligibility for Farmers: The scheme is accessible to all farmers, including sharecroppers and tenant farmers. As of 2020, participation became optional for all farmers, including those with agricultural loans.

- Crop Coverage: Includes food crops (such as cereals, millets, and pulses), oilseeds, as well as annual commercial and horticultural crops.

- Premium Structure: The premium is calculated as a percentage of the sum assured or the Actuarial Premium Rate (APR), whichever is lower. The APR is determined by the insurance providers.

- Farmer Premium Rates:

- 2% for Kharif crops

- 1.5% for Rabi crops

- 5% for commercial horticulture crops

- Farmer Premium Rates:

- Additional Features: Mandatory allocation of at least 0.5% of the total premium collected by insurance companies for Information, Education, and Communication (IEC) activities; significant reliance on technology; and states have the flexibility to select risk coverage based on their specific needs.

Key Initiatives under PMFBY

- DigiClaim: All claims are processed through the National Crop Insurance Portal (NCIP)

- CROPIC: Real-time observations and photos of crops are collected

- WINDS portal: Provides weather information network data systems

- YES-TECH Manual: Yield Estimation System based on technology

- AIDE/Sahayak: Door enrollment app for assistance

- FASAL project: Forecasting agricultural output using space, agro-meteorology, and land-based observations

- NADAMS: National Agricultural Drought Assessment and Monitoring System

- Bhuvan: ISRO's Geo-platform that provides data on plantation, pest surveillance, and weather monitoring.

PAYMENT AGGREGATOR (PA)

- PayU has obtained preliminary approval from the Reserve Bank of India (RBI) to function as a Payment Aggregator (PA).

- About Payment Aggregators (PAs)

- A financial technology company that streamlines the electronic payment acceptance process for businesses, such as Google Pay, PhonePe, and Cashfree.

- Serves as a mediator between businesses and financial institutions.

- Established as a company under the Companies Act of 1956/2013.

- Non-bank PAs must receive authorization from the RBI according to the Payment and Settlement Systems Act of 2007.

START-UPS IN RURAL INDIA

News Context

- Start-up companies are bringing hope to rural India, particularly in the agricultural sector

- Emerging start-ups are making a positive impact in rural areas of India, focusing on agriculture.

Role of Start-up in rural India

- Rural start-ups cater to the specific needs of rural communities, offering services in agri-tech, e-commerce, healthcare, and education.

Enabling Factors for Rural Start-ups:

- Internet Penetration and digital inclusion: Increased access to the internet allows rural start-ups to reach a wider audience.

- Government support: Policies and initiatives that support entrepreneurship in rural areas.

- Huge unserved customer base: Rural areas have a large population that is underserved by traditional businesses.

- Rising education level: Increased education levels in rural areas create opportunities for innovative start-ups.

- Financial inclusion: Access to financial services and funding opportunities for rural entrepreneurs.

Initiatives Undertaken

- Startup India: Launched in 2016 to support innovation and startups for economic growth.

- Startup India Seed Fund Scheme: Provides financial assistance to startups for development and commercialization.

- NewGen Innovation and Entrepreneurship Development Centre: Promotes technology-driven startups.

- Innovation & Agri-Entrepreneurship Programme: Supports agri-entrepreneurs.

- Agriculture Accelerator Fund (AAF): Provides financial support to startups in agriculture sector.

SETTLEMENT CYCLE

News Context

- SEBI has introduced a beta version of the T+0 rolling settlement cycle as an optional addition to the current T+1 settlement cycle in the Stock Markets.

- Settlement Cycle Definition: The settlement cycle is the timeframe in which securities and funds are delivered and settled after a trade is made between a buyer and a seller.

- Changes in Indian Exchanges

- Traditionally, Indian exchanges operated on a T+2 settlement cycle, meaning trades were settled two business days after the trade execution date.

- In January 2023, the settlement cycle was shifted to T+1, reducing the settlement time to one day.

- T+0 Settlement Cycle: T+0 settlement cycle refers to a system where trades are settled on the same day after the market closes.

Impact of shorten settlement cycle

- Improved Liquidity Management: With T+0 settlement, investors can quickly reinvest their funds or take advantage of new opportunities without having to wait for settlement cycles, leading to better liquidity management.

- Expanded Trading Opportunities: T+0 settlement allows investors to react swiftly to market changes, execute trades promptly, and optimize their investment strategies in real-time, providing more trading opportunities.

- Minimized Settlement Risk: By eliminating the need to wait for an extra day for trading confirmation and settlement, T+0 settlement reduces settlement risk for investors.

- Enhanced Global Competitiveness: Implementing a T+0 settlement cycle can make a market more attractive to foreign portfolio investors (FPIs), increasing global competitiveness and potentially attracting more investment.

SEBI COMPLAINT REDRESS SYSTEM (SCORES 2.0)

- The Securities and Exchange Board of India (SEBI) has launched the SCORES 2.0 version, enhancing the investor complaint resolution mechanism in the securities market by improving the efficiency of the process.

- SCORES is an online platform that allows investors in the securities market to submit their complaints via a web URL and a mobile application.

- Key features of SCORES 2.0 include:

- Shortened timelines for resolving investor complaints in the securities market, now set at 21 calendar days from the date the complaint is received.

- The introduction of auto-routing for complaints to the relevant regulated entity, which helps eliminate delays.

- Integration with the KYC Registration Agency database to facilitate easier registration.

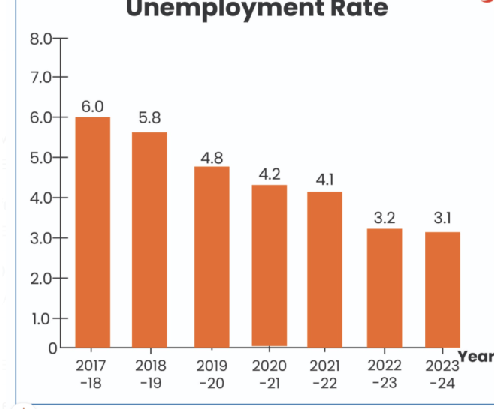

UNEMPLOYMENT IN INDIA

News Context

- Recent data from Global IIT Alumni Support Group raises concerns about unemployment in India

- Campus placements at prominent IITs are not meeting expectations

- The data suggests a potential rise in unemployment among graduates from these institutions

- This is a cause for concern in the Indian job market

Status of Unemployment in India

- Centre for Monitoring Indian Economy data shows an increase in unemployment rate from 7.4% in March 2024 to 8.1% in April 2024.

- NSSO's Periodic Labor Force Survey for Calendar Year 2023 indicates a 3.1% unemployment rate, with urban unemployment at 5.2% and rural unemployment at 2.4%.

- Women's labor force participation rate in 2023 was 41% according to PLFS data.

- World Bank's report on South Asia Development Update highlights below-average employment ratios for women in India.

- ILO's India Employment Report 2024 reveals that one out of every three unemployed individuals in India is young.

Key Employment and Unemployment indicators:

- Labor Force Participation Rate (LFPR): This indicator shows the percentage of people in the labor force, which includes those who are working or actively seeking work, in the total population. A higher LFPR indicates a larger proportion of the population is participating in the labor market.

- Worker Population Ratio (WPR): This indicator measures the percentage of employed persons in the total population. A higher WPR indicates a larger proportion of the population is employed.

- Activity Status- Usual Status: This indicator determines the activity status of individuals based on their activities in the last 365 days before the survey date. It provides a long-term perspective on employment and unemployment trends.

- Activity Status- Current Weekly Status (CWS): This indicator determines the activity status of individuals based on their activities in the last 7 days before the survey date. It provides a more short-term perspective on employment and unemployment trends.

Steps Taken towards employment generation

- Aatmanirbhar Bharat Rojgar Yojana (ABRY): Incentivizes employers to create new employment with social security benefits.

- Pradhan Mantri Mudra Yojana (PMMY): Provides collateral-free loans for micro/small businesses to set up or expand.

- PM SVANidhi Scheme: Offers collateral-free working capital loans to street vendors affected by the pandemic.

- PM Vishwakarma Scheme: Supports artisans and craftspeople in rural and urban areas.

- National Education Policy 2.0: Integrates vocational education into mainstream education to enhance employability.

- DAY-NRLM: Organizes rural women into Self Help Groups for livelihood support.

- Pradhan Mantri Kaushal Vikas Yojana: Provides industry-relevant skill training for youth.

- Others: Make in India, Start-up India, Stand-up India, Digital India, Smart City Mission, Rozgar Melas, etc.

UNCTAD REBRANDED AS UN TRADE AND DEVELOPMENT

United Nations Conference on Trade and Development (UNCTAD) has been rebranded as UN Trade and Development.

- This rebranding coincides with the organization's 60th anniversary, signaling a renewed commitment to amplifying its influence on behalf of developing nations.

- Key Achievements:

- The successful implementation of the Financing for Development initiative, as directed by the global community in the Addis Ababa Agenda (2015), in collaboration with four other major institutional partners: the World Bank, the International Monetary Fund, the World Trade Organization, and the United Nations Development Programme.

- Provided support to countries through the Debt Management and Financial Analysis System (DMFAS) Programme.

About UNCTAD

- Genesis: Originally established as a permanent intergovernmental body by the United Nations General Assembly in 1964, now rebranded as UN Trade and Development.

- Objective: To assist developing countries, especially the least developed and transitioning economies, in effectively integrating into the global economy.

- Members: Consists of 195 nations, including India.

- Functions: Helps countries address macro-level development challenges, diversify economies to reduce dependence on commodities, and minimize exposure to financial volatility.

- Organisational Structure: Substantive work is carried out by five divisions, under the leadership of the Secretary-General.

- Flagship Reports: Includes the Trade and Development Report, World Investment Report, and Digital Economy Report.

30 YEARS OF MARRAKESH AGREEMENT

The World Trade Organization (WTO) is commemorating 30 years since the signing of the Marrakesh Agreement.

- The Marrakesh Agreement was finalized in 1994 in Marrakesh, Morocco, by representatives from 123 countries following the Uruguay Round negotiations.

- This agreement led to the establishment of the WTO in 1995, replacing the General Agreement on Tariffs and Trade (GATT) as the international organization governing trade.

- Key aspects of the Marrakesh Agreement:

- It serves as the foundational framework for trade relations among all WTO members.

- It broadened the focus from trade in goods to include services, intellectual property, and other areas.

- It established a modern multilateral trading system that facilitates negotiations, dispute resolution, and economic collaboration among members.

- It laid the groundwork for the governance of the WTO, creating the Ministerial Conference (the highest decision-making body), the General Council, and specialized councils.

- WTO accomplishments include:

- Reducing trade barriers: Since 1995, the real volume of global trade has increased by 2.7 times, and average tariffs have nearly halved, dropping from 10.5% to 6.4%.

- Growth of Global Value Chains: Currently, trade within these value chains represents almost 70% of total merchandise trade.

- Development in emerging economies: There has been the fastest poverty reduction since 1995, along with rising purchasing power in various nations.

- Establishment of International Trade Agreements and Rules: These include the TRIPS Agreement, the Nairobi Package, the Trade Facilitation Agreement, and the Doha Development Agenda, among others.